Hindustan Copper Share Analysis 2025: 12.2 MTPA Expansion Target | Complete Investment Guide

Hindustan Copper Limited (HCL) भारत की एकमात्र integrated copper producer है जो mining से लेकर refining तक complete value chain में operate करती है। वर्तमान में ₹242.60 पर trading कर रहा यह stock एक unique investment proposition प्रस्तुत करता है – एक तरफ company का monopolistic position और massive expansion plans हैं, वहीं दूसरी तरफ high valuation और execution challenges भी दिखाई देती हैं। Q1 FY26 में company ने 18.4% की impressive net profit growth दिखाई है, जो copper demand की strong fundamentals को reflect करती है। HCL अब ambitious expansion plans के साथ current 4 MTPA से 12.2 MTPA capacity तक जाने का target रखा है 2030 तक, जो company को India की copper story में central player बनाएगा। यह comprehensive analysis HCL के shares की complete picture प्रस्तुत करती है, जिसमें financial performance, expansion roadmap, competitive advantages, और future growth prospects शामिल हैं।

Open-pit copper mine at Malanjkhand, Madhya Pradesh operated by Hindustan Copper Ltd.

Hindustan Copper: Company Profile और Historical Evolution

स्थापना और Legacy

Hindustan Copper Limited का establishment 9 November 1967 में हुआ था जब इसे National Mineral Development Corporation से copper-related assets transfer किए गए थे। Company एक Miniratna Category-I PSU है जो Ministry of Mines के administrative control में आती है। HCL का unique distinction यह है कि यह India की अकेली company है जो domestic copper ore mining में engaged है और देश के सभी operating copper mining leases की owner है।

Company का evolution timeline impressive है:

- 1967: Incorporation और Khetri operations का takeover

- 1972: Indian Copper Corporation (Ghatsila) का nationalization

- 1975: Khetri integrated complex की commissioning

- 1982: Malanjkhand – India की largest hard rock open pit mine

- 1989: Taloja wire rod plant की establishment

- 2015: Jhagadia secondary copper smelter का acquisition

Current Operations और Infrastructure

HCL का vertically integrated business model उसे industry में unique position देता है। Company के operations 5 states में फैले हुए हैं:

Mining Operations:

- Malanjkhand (MP): 2.5 MTPA concentrator, largest open pit mine

- Khetri (Rajasthan): Underground mining, integrated smelter-refinery

- Ghatsila (Jharkhand): Surda mine, smelter और refinery complex

Processing Facilities:

- Primary Smelter: Khetri complex

- Refineries: Khetri और Ghatsila

- Wire Rod Plant: Taloja, Maharashtra (60,000 TPA)

- Secondary Smelter: Jhagadia, Gujarat (50,000 TPA LME-A grade)

Company currently produce करती है copper concentrate, copper cathodes, continuous cast copper rods, और valuable by-products जैसे anode slime (gold, silver content), copper sulphate, और sulphuric acid।

Malanjkhand Copper Project by Hindustan Copper Limited showcasing the active copper mining site in Madhya Pradesh.

Financial Performance Deep Dive

Q1 FY26: Strong Momentum Continues

HCL ने Q1 FY26 में exceptional performance deliver की है। Net profit ₹134.28 करोड़ तक पहुंची, जो Q1 FY25 के ₹113.41 करोड़ से 18.4% का impressive growth है। यह growth primarily better copper prices और operational efficiency improvements के कारण हुई है।

Key Performance Highlights:

- Revenue Growth: ₹516.37 करोड़ (4.6% YoY growth)

- EBITDA: ₹222.29 करोड़ (13.8% YoY growth)

- EBITDA Margin: 43.1% (vs 39.6% in Q1 FY25)

- Net Profit Margin: 26.0% (excellent profitability)

- Copper Ore Production: 0.95 MMT (6.7% increase)

- EPS Growth: ₹1.39 (18.8% YoY growth)

FY25: Record-Breaking Performance

FY25 company के लिए milestone year था। Company ने highest-ever revenue from operations ₹2,070.97 करोड़ achieve किया, जो FY24 के ₹1,717 करोड़ से 21% growth दर्शाती है। Profit before tax 54% बढ़कर ₹633.51 करोड़ तक पहुंची, जबकि PAT 42% growth के साथ ₹468.53 करोड़ रही।

Balance Sheet Strength और Capital Structure

HCL की balance sheet fundamentally strong है। Company का debt-to-equity ratio केवल 0.06 है, जो excellent financial health indicate करती है। Total debt levels significantly reduce हुई हैं recent years में। Share capital steady ₹483.51 करोड़ पर stable है, जबकि reserves impressive growth से ₹1,801.58 करोड़ तक पहुंची हैं।

Key Balance Sheet Metrics:

- Net Worth: Strong equity base with growing reserves

- Current Ratio: 1.37 (adequate liquidity)

- ROE: 17.58% (excellent returns)

- ROA: 13.37% (efficient asset utilization)

- Book Value per Share: ₹27.55 (16.6% YoY growth)

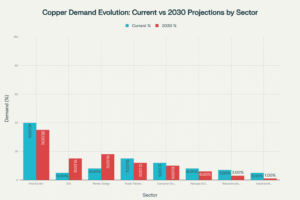

Copper demand का sector-wise breakdown – current vs 2030 projections

The Copper Demand Revolution: Structural Growth Story

India’s Copper Consumption Trajectory

India की domestic refined copper demand healthy 11% growth rate maintain कर रही है FY25 में, जो global growth rate से significantly higher है। यह growth infrastructure development और renewable energy transition की वजह से driven है। Current domestic consumption around 850,000 MT annually है, जबकि production केवल 497,000 MT है।

Demand Drivers Analysis:

- Infrastructure & Construction: 40% current share, smart cities और housing schemes

- Electric Vehicles: 5% current but 25% growth rate expected

- Renewable Energy: 8% share with 20% growth potential

- Power Transmission: 15% share, grid modernization driving demand

Green Energy Transition: Copper’s Golden Age

Copper demand का biggest catalyst है global energy transition। As per industry estimates, India की copper demand 3-3.3 million MT तक reach करेगी 2030 तक और 9.8 million MT तक 2047 तक। यह massive demand creation का opportunity है HCL के लिए।

EV Revolution Impact: Electric vehicles में copper usage conventional vehicles से 4x ज्यादा है। India का EV adoption target और charging infrastructure development copper demand को significantly boost करेगा। Renewable Energy Surge: Solar panels, wind turbines, और grid infrastructure में copper की indispensable requirement है। India का renewable energy capacity target 500 GW by 2030 copper consumption को exponentially increase करेगा।

Expansion Roadmap: 12.2 MTPA Vision

Ambitious Capacity Expansion Plan

HCL का most exciting aspect है इसकी ambitious expansion strategy। Company ने target किया है current 4 MTPA से 12.2 MTPA तक capacity increase करना 2030-31 तक। यह tripling of capacity massive investment और execution capability require करती है।

Investment Timeline:

- Total Investment: ₹2,000+ करोड़ over 5-6 years

- Phase 1: Existing mines expansion (2025-26)

- Phase 2: New mines development (2026-28)

- Phase 3: International exploration (2025-30)

Major Projects Pipeline

1. Rakha Mine Reopening:

Company ने South West Mining Ltd (SWML) को 20-year MDO contract award किया है Rakha copper mine को reopen करने के लिए। Total CAPEX ₹2,700 करोड़ है और expected capacity addition 1.5 MTPA है। यह project significant employment generation भी करेगा (10,000 direct+indirect jobs)।

2. Malanjkhand Expansion:

Current 2.5 MTPA capacity को expand करके additional capacity create करने की plans हैं। नया ₹400 करोड़ का 3 MTPA concentrator plant भी planned है।

3. New Concentrator Plants:

- Malanjkhand में 3 MTPA plant (₹400 करोड़)

- Rakha में 3 MTPA plant (₹300 करोड़)

- Construction start expected next year

4. International Expansion:

HCL ने Chile’s CODELCO के साथ historic MoU sign किया है knowledge sharing और technology transfer के लिए। Company India के top executives को Chile भेज रही है CODELCO की world-class mines की study के लिए।

Open-pit copper mining operation showcasing terraced excavation layers in India.

Competitive Landscape और Market Position

HCL’s Unique Advantages

HCL का competitive position exceptionally strong है domestic copper sector में। Company के पास several unique advantages हैं:

1. Monopolistic Mining Position: HCL अकेली company है India में जो domestic copper ore mining करती है। सभी other players import-dependent हैं।

2. Integrated Operations: Complete value chain control mining से refining तक gives cost and quality advantages।

3. Government Support: PSU status से policy support, funding access, और regulatory favor।

4. Strategic Asset Base: Prime mineral-rich land holdings और established infrastructure।

Competitive Comparison

Indian copper industry में 3 major players dominate करते हैं:

Market Share Analysis:

- Hindalco Industries: 38% market share, large import-based operations

- Vedanta (Sterlite): 25% share, currently facing operational challenges

- HCL: 10% share but only domestic miner

- Others: 27% including new entrants like Adani Kutch Copper

Key Differentiators:

- Hindalco: Scale advantages, established distribution

- Vedanta: Technology expertise, global operations (when operational)

- HCL: Domestic mining advantage, government support

- Adani: Modern facilities, aggressive expansion plans

Import Dependency Challenge

India imports over 90% of its copper concentrates, जो 97% तक increase होने expected है 2047 तक। यह massive opportunity है HCL के लिए domestic production increase करने का। Current import bill substantial है और geopolitical risks भी create करती है।

Strategic Partnerships और International Collaboration

CODELCO Partnership: Game Changer

HCL का partnership with Chile’s CODELCO (world’s largest copper producer) strategic masterstroke है। CODELCO team की 3-week India visit recent में हुई है सभी HCL units की assessment के लिए। Key collaboration areas include:

- Technology Transfer: Modern mining techniques और equipment

- Operational Excellence: Best practices sharing और efficiency improvement

- Safety Standards: World-class safety protocols implementation

- Capacity Building: Employee training और skill development

Joint Ventures with PSUs

HCL ने strategic partnerships बनाए हैं various PSUs के साथ critical minerals exploration के लिए:

- IOCL & GAIL: Critical minerals blocks bidding

- RITES: Supply chain development

- Coal India: Chile exploration projects

यह partnerships HCL को broader mineral portfolio और international exposure देंगे।

Copper smelting facility with industrial machinery and workers inside a refinery plant.

Risk Assessment और Challenges

Operational Risks

1. Commodity Price Volatility:

Copper prices highly volatile हैं international markets में। FY2023 में average price $8,000/MT था, लेकिन 15% decline भी देखी गई Q2 में demand concerns के कारण। यह volatility company की profitability को significantly impact करती है।

2. Execution Risk:

Ambitious expansion plans की execution major challenge है। ₹2,000+ करोड़ का CAPEX program require करता है excellent project management और timely approvals। Past में delays हुई हैं similar projects में।

3. Operational Challenges:

Mining operations face करते हैं equipment failures, labor issues, और safety incidents। Q1 FY2024 में 8% production decrease हुई थी maintenance issues के कारण।

Regulatory और Environmental Risks

Mining Industry Regulation:

Heavy regulatory oversight और changing environmental norms operational costs बढ़ा सकते हैं। New Mineral Laws Amendment Act 2021 के implications royalty payments और resource allocation पर impact डाल सकते हैं।

Environmental Compliance:

Stricter environmental regulations और sustainable mining practices की requirement compliance costs increase कर सकती है। Underground mining operations environmental impact को mitigate करती हैं, लेकिन फिर भी regulatory oversight बढ़ रही है।

Competition और Market Risks

Private Sector Competition:

Hindalco और Vedanta जैसे established players के साथ competition intensifying है। नए entrants जैसे Adani Kutch Copper भी market dynamics change कर रहे हैं।

Technology Gap:

Modern mining techniques और processing technology में investment की requirement है competitiveness maintain करने के लिए। Vintage plants जैसे Ghatsila smelter-refinery adverse cost structure रखते हैं।

Valuation Analysis: Premium या Justified?

Current Valuation Metrics

HCL के current valuation metrics mixed signals देते हैं:

- P/E Ratio: 47.72 (high compared to sector)

- P/B Ratio: 8.74 (premium to book value)

- Market Cap: ₹23,194 करोड़

- EV/EBITDA: Higher multiples due to growth expectations

- Dividend Yield: 0.38% (low payout)

Valuation Justification Factors

Growth Premium:

High valuation partially justified है aggressive expansion plans और tripling capacity targets के कारण। 12.2 MTPA achievement successful होने पर significant value creation expected है।

Scarcity Value:

Being India की only domestic copper miner gives scarcity premium। Import substitution theme और self-reliance focus further supports valuation।

Sectoral Tailwinds:

Copper demand की structural growth story valuation premiums को support करती है। EV adoption और renewable energy transition long-term growth visibility provide करते हैं।

Price Target Analysis

Analysts का consensus mixed है current valuation levels पर:

- 2025 Target: ₹306-431 range

- 2026 Target: ₹443-624 range

- 2030 Target: ₹1,957-2,755 range (bullish scenarios)

यह targets assume करते हैं successful capacity expansion, commodity price stability, और execution excellence।

Dividend Policy और Shareholder Returns

Historical Dividend Pattern

HCL का dividend history relatively modest है। Current dividend yield 0.38% है industry average से lower। Recent dividend payments:

- FY25: ₹1.46 per share

- FY24: ₹0.92 per share

- FY23: ₹0.92 per share

- FY22: ₹1.16 per share

Payout Policy

Company का dividend payout ratio around 30% maintain रहा है earnings का। Management focus करती है growth investments पर rather than high dividend payouts। यह strategy justified है current expansion phase को considering।

Retention Strategy:

High earnings retention (69.89%) supports internal funding of expansion projects। Company avoid करना चाहती है excessive debt funding को high CAPEX requirements के लिए।

Future Growth Catalysts और Strategic Outlook

Demand-Supply Gap Opportunity

India की copper demand और domestic production के बीच massive gap है। Current import dependency 90%+ है, जो significant opportunity represents करती है HCL के लिए। Successful capacity expansion import substitution में help कर सकती है।

Technology Modernization

CODELCO partnership से technology upgradation expected है। Modern mining techniques, automation, और efficiency improvements operational costs reduce कर सकते हैं और productivity बढ़ा सकते हैं।

Green Mining Initiatives

Sustainable mining practices और environmental compliance में investment company को regulatory advantages दे सकती है। Underground mining focus environmental impact को minimize करती है।

International Expansion

Chile exploration projects और critical minerals diversification HCL को broader resource base दे सकते हैं। यह geographic और commodity diversification strategic advantage है।

Investment Thesis और Recommendations

Bull Case Scenario

Positive Catalysts:

- Successful execution of 12.2 MTPA expansion plan

- Copper demand surge from EV और renewable energy adoption

- Import substitution opportunity in domestic market

- Technology upgradation through CODELCO partnership

- Government support for domestic mining और self-reliance

- Strong balance sheet और low debt levels

Bear Case Scenario

Risk Factors:

- Execution challenges में delays या cost overruns

- Copper price volatility affecting profitability

- Competition intensification from private players

- Regulatory hurdles में project approvals

- High current valuation limiting upside potential

- Technology gap compared to global peers

Investment Recommendation

For Growth Investors: HCL में investment opportunity है long-term copper demand story के लिए। Expansion success पर significant value creation possible है।

For Value Investors: Current valuation levels stretched appear करती हैं near-term के लिए। Better entry points possible हैं corrections पर।

For Income Investors: Low dividend yield makes यह unsuitable income-focused portfolios के लिए।

For Sector Play: Copper sector exposure के लिए HCL unique domestic mining advantage रखती है।

निष्कर्ष: India की Copper Story का Central Player

Hindustan Copper Limited India की copper industry में unique position रखती है – यह देश की अकेली integrated domestic copper producer है जो mining से refining तक complete value chain control करती है। Company का current moment particularly exciting है क्योंकि यह massive transformation के दौर से गुजर रही है।

Key Investment Highlights:

Monopolistic Position: India में domestic copper ore mining में HCL का exclusive position strategic moat है। जबकि सभी competitors import-dependent हैं, HCL self-reliant है।

Massive Expansion Opportunity: 4 MTPA से 12.2 MTPA capacity expansion successful होने पर company की revenue और profitability को exponentially बढ़ा सकती है।

Structural Demand Growth: Copper demand की underlying fundamentals exceptionally strong हैं। EV revolution, renewable energy transition, और infrastructure development सभी copper consumption को support करते हैं।

Government Support: PSU status और self-reliance focus से policy support guaranteed है। Critical minerals strategy में HCL central role play करेगी।

Strategic Partnerships: CODELCO के साथ partnership technology और operational excellence में quantum jump ला सकती है।

Key Investment Concerns:

Execution Risk: Ambitious expansion plans की successful execution critical है। Past track record mixed है और project delays possible हैं।

High Valuation: Current P/E 47+ levels पर entry risky हो सकती है। Better valuations के लिए wait करना prudent हो सकता है।

Commodity Volatility: Copper prices की volatility earnings predictability को affect करती है।

Competition Pressure: Private players का scale advantage और operational efficiency competition create करते हैं।

Investment Strategy Recommendation:

Aggressive Investors: 3-5% portfolio allocation justify हो सकती है long-term growth potential के लिए। Successful expansion story पर substantial returns possible हैं।

Conservative Investors: Current valuation levels पर wait करना बेहतर है। 20-30% correction पर attractive entry point मिल सकती है।

Sector Diversification: Copper exposure के लिए HCL unique proposition है domestic mining advantage के साथ।

Long-term Perspective: यह 5-10 year investment story है quick returns के लिए suitable नहीं है। HCL ultimately India की copper self-sufficiency और energy transition story का integral part है। Company का success India के strategic objectives align करती है, लेकिन execution excellence और market timing crucial factors रहेंगे investment returns के लिए। Investors को balanced approach अपनाना चाहिए जो growth potential को recognize करे लेकिन execution risks को भी acknowledge करे।

Disclaimer: यह analysis educational purpose के लिए है। Investment decisions से पहले professional financial advice लें और अपनी risk appetite consider करें।

आपने कभी stocks में invest किया है? आपका experience कैसा रहा?

इस post को उन दोस्तों के साथ share करें जो investing में interested हैं। इस post को अपने WhatsApp groups में share करें और अपने friends की financial literacy बढ़ाने में help करें!”

- Comment section में अपना investment experience share करें – आपकी story दूसरों की help कर सकती है!”

- “आपके कोई questions हैं? Comment में पूछें, मैं personally reply करूंगा।”

- Also Read :

- NTPC Green Energy में निवेश करें या नहीं? क्या यह अगला मल्टीबैगर है?2025

- ONGC का भविष्य: 2025 में ग्रोथ, चैलेंज और अपॉर्च्युनिटी का एनालिसिस

- Easy My Trip शेयर की पूरी जानकारी 2025 | Travel Stock Guide

- HCL Infosystems शेयर में निवेश करना चाहिए या नहीं 2025 ||